Cash Flow Management for Pet Care Businesses: Survive Crunches and Build Long-Term Stability

Table of Contents

About the Author

Jeremy

Petcare Sales Manager

Passionate about helping pet businesses thrive through technology and innovation.

Why Cash Flow Is the #1 Killer of Profitable Pet Businesses

You can be fully booked every week, charge fair prices, and still run out of money. It sounds contradictory, but it happens to pet care businesses all the time — groomers, boarders, daycare owners, trainers, and vets alike. The culprit is almost never profit. It's cash flow.

Cash flow is the movement of money into and out of your business. Profit is a number on a spreadsheet. Cash flow is what pays your rent, your staff wages, your supplier invoices, and your own salary this Friday. A business can be technically profitable and still fail because it ran dry waiting for money to arrive.

In the pet care industry, cash flow challenges are especially common because of seasonality (summer boarding peaks, January lulls), irregular client payment habits, upfront product and supply costs, and the high cost of staff relative to revenue. Understanding how to manage cash flow — and what to do when it tightens — can be the difference between a business that survives a tough quarter and one that closes its doors.

This guide gives you a practical, step-by-step framework: how to read your cash flow clearly, how to build resilience, and exactly what levers to pull when you hit a crunch.

Understanding Your Cash Flow: The Basics Every Pet Business Owner Needs to Know

Before you can manage cash flow, you need to understand what's flowing in and what's flowing out — and when. This is more nuanced than it sounds.

Cash inflows for a pet business typically include: client payments for services (grooming, boarding, daycare, training, vet consultations), product retail sales, package or membership prepayments, gift voucher purchases, and any grants or loans received.

Cash outflows include: rent and utilities, staff wages and payroll taxes, pet food and supply purchases, cleaning and hygiene products, software subscriptions, insurance premiums, loan repayments, marketing spend, and your own owner's draw.

The key metric to track is net cash position over time — not just whether you're profitable, but whether you'll have enough money in the bank to cover your bills each week and month. A simple cash flow forecast (a spreadsheet or tool that projects expected inflows and outflows over the next 4–12 weeks) gives you visibility and time to react before a crunch hits.

Most pet business owners manage by gut feel and bank balance. The ones who build lasting businesses learn to manage by forward visibility. You want to know three weeks in advance that you're going to be short — not three days after your rent bounced.

The 5 Most Common Cash Flow Mistakes Pet Business Owners Make

Most cash flow problems are avoidable. They're the result of patterns that feel manageable in the short term but compound into crises. Here are the five mistakes that trip up pet businesses most often:

1. Mixing business and personal finances. When your personal spending and business spending come from the same account, it's nearly impossible to see what your business actually costs to run. Open a dedicated business bank account from day one and pay yourself a defined owner's draw rather than dipping in whenever you need money.

2. Failing to track payment timing. Knowing you're owed £3,000 this month is meaningless if clients pay on day 30 and your payroll goes out on day 15. Map not just what you're owed but when it will actually arrive. Late or inconsistent client payments are a structural problem, not a one-off inconvenience.

3. No cash reserve buffer. Most financial advisers recommend holding 1–3 months of operating expenses in a separate savings account. Most small pet business owners hold far less — sometimes nothing. Without a buffer, a single slow week can cascade into a crisis.

4. Underpricing services relative to true costs. If your prices don't account for all your actual costs (including your own time at a realistic wage), you're slowly draining your reserves with every appointment. Cash flow pressure often signals a pricing problem underneath.

5. Seasonal blindness. If you've been in the pet industry for more than a year, you know January is quieter than December. If you know this and don't set aside surplus cash from peak seasons to cover off-peak months, you'll face a crunch every year — reliably and predictably — even though it's completely foreseeable.

Building a Cash Flow Forecast: A Simple Framework for Pet Service Providers

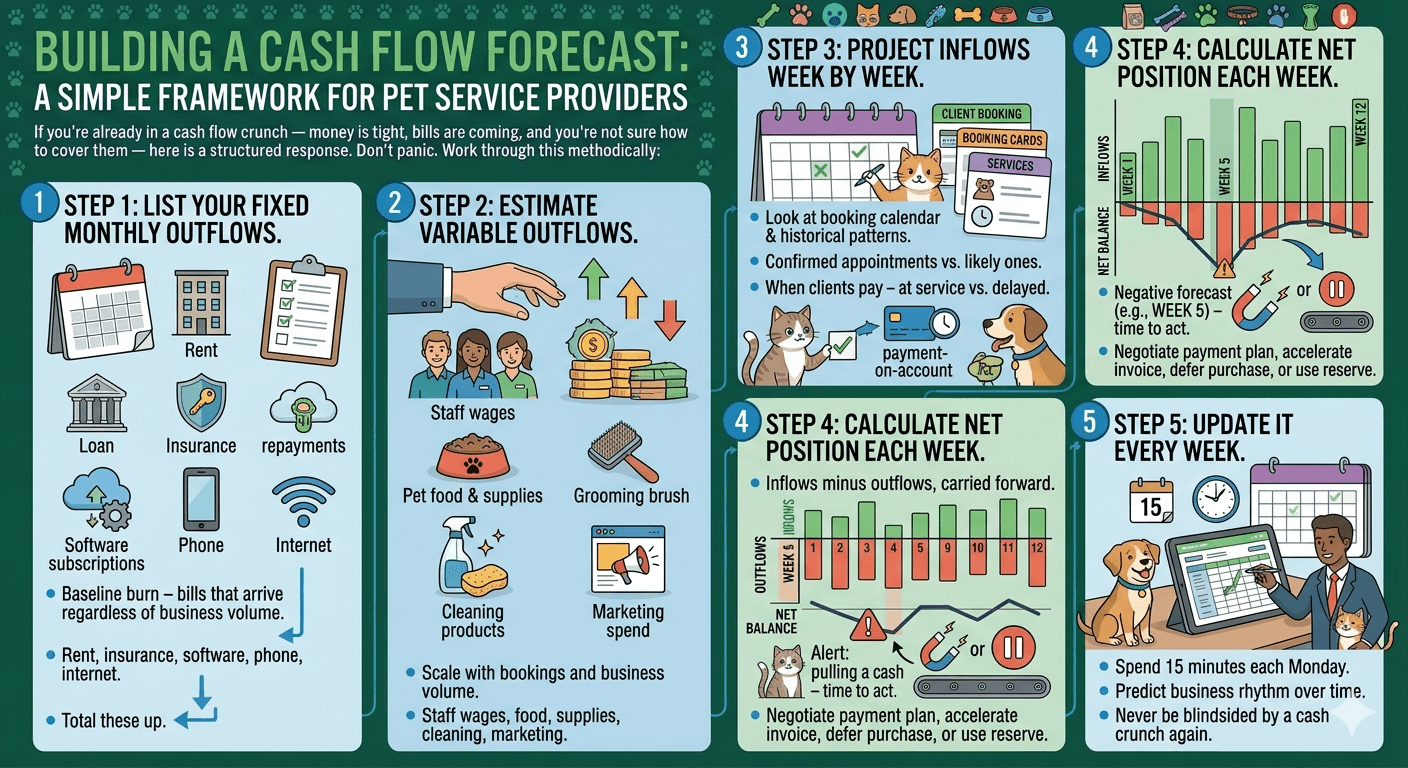

A cash flow forecast doesn't have to be complex. A basic 12-week rolling forecast can transform how you run your business. Here's how to build one:

Step 1: List your fixed monthly outflows. These are bills that arrive regardless of how busy you are: rent, insurance, loan repayments, software subscriptions, phone, internet. Total these up. This is your baseline burn — the minimum amount of cash you need flowing in each month before you've paid a single member of staff or bought a single bag of food.

Step 2: Estimate variable outflows. Staff wages (especially if you use part-time or casual staff who scale with bookings), pet food and supplies, cleaning products, and marketing spend. These rise and fall with business volume, so estimate based on expected bookings.

Step 3: Project inflows week by week. Look at your booking calendar and client records. How many appointments are confirmed? How many are likely based on your historical patterns? When will each client pay — at time of service, or on account with delay?

Step 4: Calculate net position each week. Inflows minus outflows, carried forward into the next week. If your projection shows a negative balance coming in week 5, you have time to act — negotiate a payment plan, accelerate a client invoice, defer a non-essential purchase, or draw on your reserve.

Step 5: Update it every week. A forecast is only useful if it reflects reality. Spend 15 minutes each Monday updating it. Over time you'll get better at predicting your business rhythm, and you'll never be blindsided by a cash crunch again.

5 Proactive Strategies to Strengthen Your Cash Flow Before a Crunch Hits

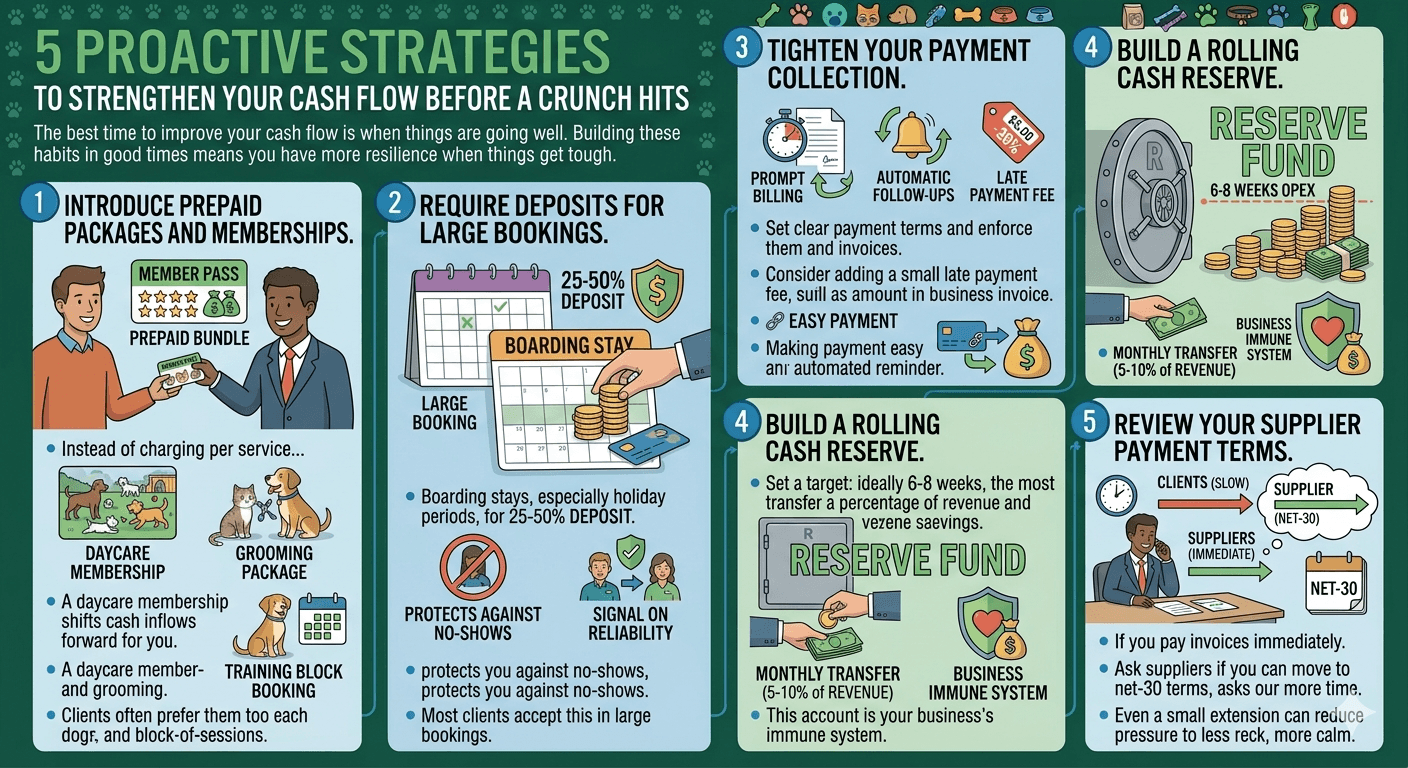

The best time to improve your cash flow is when things are going well. Building these habits in good times means you have more resilience when things get tough.

1. Introduce prepaid packages and memberships. Instead of charging per service, offer clients the option to pay upfront for a bundle of sessions or a monthly membership plan. This shifts cash inflows forward — you receive payment before you've delivered the service. A daycare membership, a grooming package, or a training block booking all serve this purpose. Clients often prefer them too, because they feel like they're getting value.

2. Require deposits for large bookings. Boarding stays, especially holiday periods, should require a 25–50% deposit at time of booking. This protects you against no-shows and brings cash in earlier. Most clients accept this as standard practice — and if they don't, that's a signal about how reliable they're likely to be.

3. Tighten your payment collection. If you run any form of account or invoice-based billing, set clear payment terms and enforce them. Send invoices promptly. Follow up on late payments without hesitation. Consider adding a small late payment fee for invoices unpaid beyond 14 days. Making payment easy — card on file, online payment links, automated reminders — reduces friction and speeds up collection.

4. Build a rolling cash reserve. Set a target: ideally 6–8 weeks of operating expenses held separately. Each month, transfer a percentage of revenue (even 5–10%) into a dedicated reserve account. Don't touch it except for genuine emergencies. This account is your business's immune system.

5. Review your supplier payment terms. If you pay invoices immediately but your clients pay you slowly, you're funding a gap. Ask suppliers if you can move to net-30 terms rather than paying on delivery. Even a small extension in your payables can reduce pressure significantly.

Warning Signs: How to Spot a Cash Flow Crunch Before It Hits

A cash flow crunch rarely arrives without warning. Learn to read the early signals so you can act before things become critical:

You're checking your bank balance nervously before approving any purchase — even routine ones. You're delaying supplier payments beyond their due dates. You're using a business credit card or overdraft regularly to cover operating costs, not one-off investments. You're avoiding opening financial emails or statements. Staff wages feel precarious to make each pay cycle. These are not signs of bad luck. They're signs of a structural cash flow problem that needs deliberate attention.

Other warning signs include: a sudden drop in bookings without a corresponding drop in overheads; a large client who represents a disproportionate share of your income going quiet; an unexpected large expense hitting (equipment repair, vet bill for a boarded animal, staff sick leave) without reserve to absorb it; or a seasonal trough you didn't plan for arriving on schedule.

The Cash Flow Crunch Playbook: What to Do When You're Already in One

If you're already in a cash flow crunch — money is tight, bills are coming, and you're not sure how to cover them — here is a structured response. Don't panic. Work through this methodically:

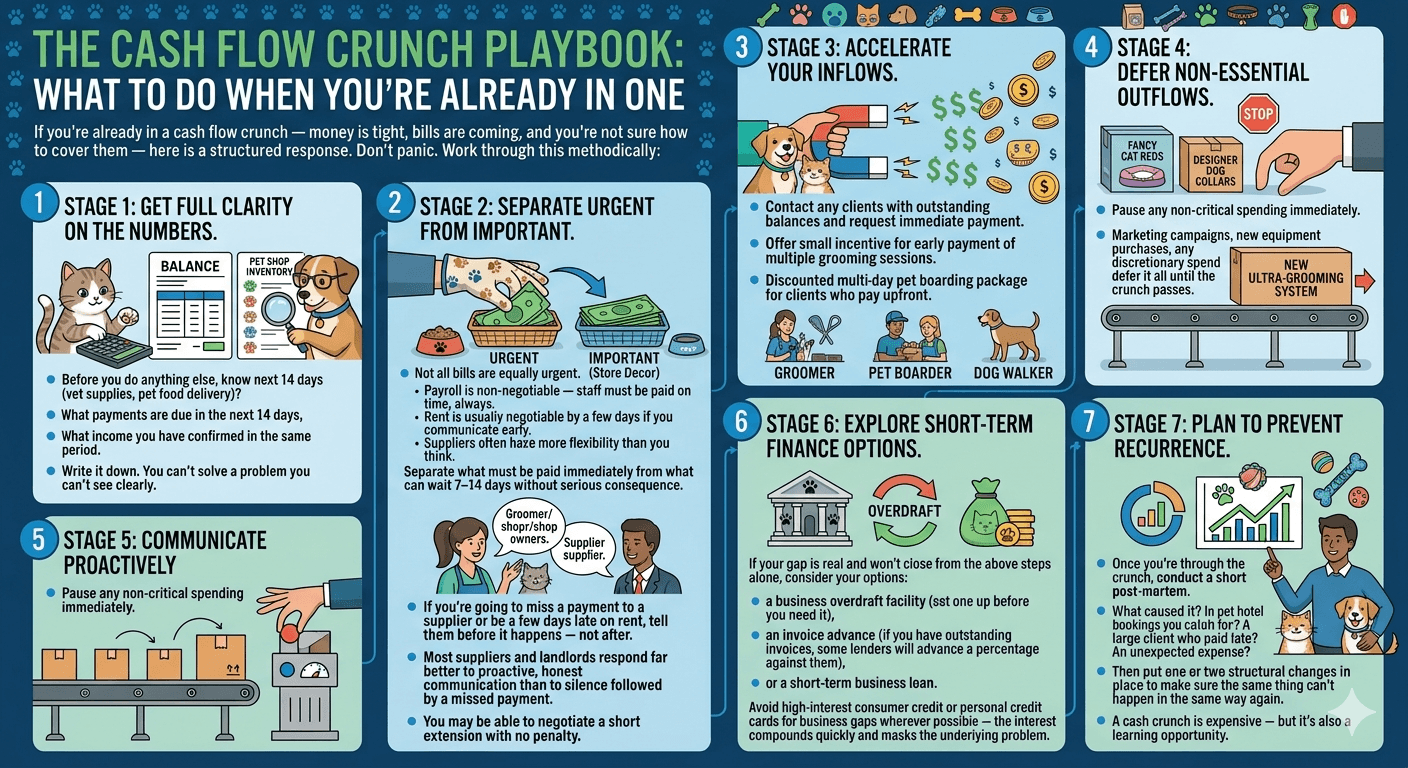

Stage 1: Get full clarity on the numbers. Before you do anything else, know exactly how much cash you have right now, what payments are due in the next 14 days, and what income you have confirmed in the same period. Write it down. You can't solve a problem you can't see clearly.

Stage 2: Separate urgent from important. Not all bills are equally urgent. Payroll is non-negotiable — staff must be paid on time, always. Rent is usually negotiable by a few days if you communicate early. Suppliers often have more flexibility than you think. Separate what must be paid immediately from what can wait 7–14 days without serious consequence.

Stage 3: Accelerate your inflows. Contact any clients with outstanding balances and request immediate payment. Offer a small incentive for prepayment of future services. Run a short-term promotion — a discounted package for clients who pay upfront this week. If you have gift vouchers, promote them. Cash in hand today is worth more than revenue next month.

Stage 4: Defer non-essential outflows. Pause any non-critical spending immediately. Marketing campaigns, new equipment purchases, any discretionary spend — defer it all until the crunch passes. Review every outgoing and ask: does this need to happen this week, or can it wait 30 days?

Stage 5: Communicate proactively with key parties. If you're going to miss a payment to a supplier or be a few days late on rent, tell them before it happens — not after. Most suppliers and landlords respond far better to proactive, honest communication than to silence followed by a missed payment. You may be able to negotiate a short extension with no penalty.

Stage 6: Explore short-term finance options. If your gap is real and won't close from the above steps alone, consider your options: a business overdraft facility (set one up before you need it), an invoice advance (if you have outstanding invoices, some lenders will advance a percentage against them), or a short-term business loan. Avoid high-interest consumer credit or personal credit cards for business gaps wherever possible — the interest compounds quickly and masks the underlying problem.

Stage 7: Plan to prevent recurrence. Once you're through the crunch, conduct a short post-mortem. What caused it? A seasonal dip you didn't plan for? A large client who paid late? An unexpected expense? Then put one or two structural changes in place to make sure the same thing can't happen in the same way again. A cash crunch is expensive — but it's also a learning opportunity.

Seasonal Cash Flow Planning for Pet Care Businesses

The pet care industry has highly predictable seasonal patterns. If you've operated for a year or more, you have data. Use it.

For most UK and Australian pet businesses, peak demand arrives in December (boarding and daycare surge), school holiday periods, and warmer months (grooming demand rises). Quiet periods typically arrive in January, after school holidays end, and mid-week in general service demand.

The strategy is simple: during peak periods, build your reserve. During quiet periods, draw on it. This sounds obvious, but most business owners spend their peak-period surplus and then struggle through the quiet months. Treat your peak income as partially deferred — earmark a portion of it as "quiet period buffer" from the moment it arrives.

Build a simple seasonal calendar for your business: mark your historically busiest and quietest months, estimate the difference in revenue between your best and worst months, and calculate how much you need in reserve to bridge the quiet periods without stress. Then build toward that number systematically.

You can also offset seasonality by diversifying your services. A groomer who adds nail trims and de-shedding treatments sees more consistent bookings. A boarder who offers daycare has a more even daily revenue stream. A dog trainer who sells online courses generates income even when face-to-face sessions are slow. Strategic service expansion isn't just about growth — it's also about cash flow smoothing.

How the Right Software Can Transform Your Cash Flow Visibility

One of the most powerful things a pet business owner can do for their cash flow is improve their financial visibility — and the right software makes this dramatically easier.

A good pet business management platform gives you real-time visibility into bookings, revenue, outstanding payments, and client payment history. You can see at a glance who owes you money, which clients have credit on account, and what your expected revenue looks like for the next 4 weeks. That kind of visibility is the foundation of good cash flow management.

Beyond visibility, automation matters. Software that sends automatic payment reminders, enables clients to pay online at time of booking, and stores card details for frictionless recurring charges dramatically shortens your payment collection cycle. Instead of chasing invoices, money arrives promptly and predictably.

Package and membership management features allow you to sell prepaid service bundles — bringing cash in before you deliver the service and smoothing your revenue across weeks and months. Reporting tools let you track revenue trends, identify your busiest and quietest periods, and build accurate cash flow forecasts based on real data rather than guesswork.

The pet businesses that manage cash flow best are almost always the ones that have replaced manual spreadsheets and paper records with integrated digital systems. The visibility and automation that good software provides doesn't just save time — it directly improves your financial health.

Pricing, Profitability, and the Cash Flow Connection

It bears repeating:

chronic cash flow pressure is often a symptom of a pricing problem. If you're consistently stretched, consistently deferring supplier payments, and consistently unable to build a reserve — even in your busiest periods — your prices may not reflect the true cost of running your business.

Calculate your true cost per service.

Include: your time at a rate that reflects what your time is worth, all materials and supplies, a proportional share of overheads (rent, insurance, software, marketing), and a contribution toward your cash reserve and equipment replacement fund. If your prices don't cover all of this and leave you with a margin, you're undercharging.

Raising prices is uncomfortable.

Most pet business owners fear losing clients. In practice, a modest price increase — applied thoughtfully, communicated clearly, and backed by genuine quality of service — rarely causes significant client attrition. And the clients who leave over a 5–10% price increase are often the ones who were never going to be loyal, high-value clients anyway.

Price your services to be sustainable, not just competitive.

A business that charges slightly more but remains open, well-staffed, and financially stable serves its clients far better than one that burns out its owner, cuts corners on quality, and eventually closes.

Take Control of Your Cash Flow With GoPetAI

Cash flow management doesn't have to be a constant source of anxiety. With the right habits, the right tools, and a clearer picture of your numbers, you can build a pet care business that's not just busy but financially stable and resilient.

GoPetAI is built for pet care service providers who want to work smarter, not harder. Our platform gives you real-time booking and revenue visibility, automated client payment collection, prepaid package and membership management, and the reporting tools you need to forecast and manage your cash flow with confidence.

Whether you run a grooming salon, boarding facility, daycare centre, or mobile pet service, GoPetAI helps you get paid faster, plan better, and sleep easier knowing your finances are under control.

Ready to take control of your cash flow? Explore GoPetAI today and discover how the right platform can transform the financial health of your pet care business.

Related Articles

Cattery Management Software: The Complete Guide for Modern Pet Boarding Businesses

9 min

Loyalty Cards, Referral Programs, Coupons and Gift Certificates: The Pet Business Guide to Repeat Sales and New Clients

23 min

Why Your Australian Pet Business Needs Online Booking in 2026 (And How to Set It Up)

7 min